Q4(Jan – Mar 2023)real GDP growth rate (2nd preliminary seasonally adjusted series values):YoY0.4%

Q4 real GDP (2nd preliminary values):138 trillion 550.6 billion JPY / YoY1.3% (Source:Cabinet Office)

The May 2023 edition of the MARE Monthly Real Estate Market Report will be divided into the following chapters.

1. Summary on the Change of Governors of the old and new Bank of Japan and 'Achieving a Virtuous Cycle of Growth and Distribution'; 2. Information on the Real Estate Market: Basic Data on a Real Economy; 3. Information on Property Market Trends: Economic Outlook; and 4. Prospects for Future Property Purchases. Of the above, in section 1 we will look at the current state of wage increases in large, medium and small sized enterprises.

We hope that this will help readers to understand the opportunities for buying and selling property.

【1.Summary on the Change of Governors of the old and new Bank of Japan and 'Achieving a Virtuous Cycle of Growth and Distribution'.】

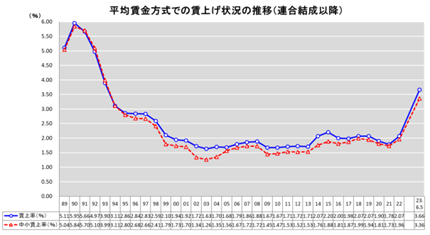

Last month's issue described business climate in the private sector, with a focus on planned wage increases and an increase in the number of bankruptcies. In this issue, we review the 10 years of the Kuroda era following the retirement of former Bank of Japan Governor Kuroda on 8 March. It also provides an insight into the results of the Cabinet's Consultative Meeting on Economic and Fiscal Policy ('Cabinet Advisory Council'), which was held on 30 March and 18 April respectively to confirm the Government's economic policy, and its impact on the Japanese economy, including the real estate industry, going forward.

During the 10-year tenure of former BOJ Governor Kuroda, the main policy was the introduction of "other-dimensional easing", which was summarised by increasing the balance of long-term government bonds by JPY 50 trillion per year, increasing the balance of listed investment trusts by JPY 1 trillion and implementing large-scale asset purchases to increase the BOJ's debt monetary base by JPY 60 trillion to JPY 70 trillion per year. As a result, the excessive appreciation of the yen was curbed, stock prices rose and corporate capital increased significantly, while capital investment did not grow significantly, labour participation rates fell and wage growth was poor. In addition, negative aspects of the lessons learned were that interest rates on government bonds fell sharply, which put pressure on bank profits, and the loosening of fiscal discipline caused productivity to stagnate and real wages to be pushed down. As mentioned in last month's issue, the impact of wage increases this spring was significant, but the latest real wage growth rate remains well below the rate of price growth, which was affected by external factors, down 2.9% YoY. At first glance, the current price growth rate of more than 2% appears to be reaching the target of the annual "2% rise" set by former Governor Kuroda, but in reality, the increase is mainly driven by external factors such as higher resource prices and higher imports of products due to the rapid depreciation of the yen. Without sufficient wage growth, a virtuous cycle in the economy will not be created, and it will be extremely difficult to achieve the price target in a stable manner, even with the continuation of interdimensional easing. This 'realisation of a virtuous circle of growth and distribution' was the main theme of the last two meetings of the Cabinet Advisory Council.

At the 30 March meeting, the main obstacles to growth were the abnormal excess savings of companies and the low labour share. The need for sustained wage increases and the importance of improving labour productivity, labour share and terms of trade for this. The need for 'smart spending', reductions in cost-effective small expenditures, curbs on social security spending and fiscal consolidation from normal times in preparation for crises in order to realise MSSE (Modern Supply-Side Economics), where the government plays a certain role, rather than the traditional 'small government' economic policy in a difficult fiscal situation. The government has been working on a number of measures to improve the financial health of the country. The objective was to continue the policy blending between the market and the government, with the market economy and the government correcting its failures. It then stated that excessive expansion of government debt should be avoided while investing in infrastructure, childcare, education and global warming prevention.

At a meeting of the Cabinet Advisory Council on 18 April, new BOJ Governor Ueda stated that the BOJ would "firmly carry out stable monetary management". At the same meeting, he also stated that a virtuous cycle between wages and prices had already started in spring 2022 and that a strategy was needed to consolidate this virtuous cycle by 2025. He further explained the need to formulate policy targets using macro indicators and KPIs and to check policy implementation in order to realise the central goal of the new capitalism: sustainable growth in terms of income. Inward FDI is very important for this, he said, and it is essential to create an environment where not only investment but also the accompanying foreign technology and excellent human resources can enter Japan, and where technology and ideas can be exchanged both domestically and internationally. The report concludes, however, that this should be accompanied by a review of the system, including the taxation system.

The following section reviews the actual economic situation surrounding the property market.

【2.Property Market Related Information: Basic Data on a Real Economy】

In the following section, basic real economy information is reviewed.

Table 1 shows that new housing starts increased by 9,267 units MoM, but showed a YoY decline of 3.2% to 73,693 units, indicating a decrease. The breakdown was 17,484 owner-occupied units, down 13.6% YoY, showing a decrease for the 16th consecutive month, while 32,585 houses for rent increased by 0.9% YoY, showing an increase for the 25th consecutive month. The number of houses for sale decreased by 0.4% YoY to 23,053, marking the second consecutive month of year-on-year decline. Owner-occupied dwellings decreased for the 15th consecutive month, with 15,950 units privately financed, down 14.0% YoY, and for the 17th consecutive month, with 1,534 units publicly financed, down 10.2% YoY, representing a decline for owner-occupied dwellings overall. For houses for rent, the number of privately financed houses decreased by 29,069 or 0.7%, the first decline in nine months, while publicly financed houses increased by 3,516 or 16.2%, the second consecutive monthly increase. Among condominiums for sale, condominiums increased for the fourth consecutive month with 11,378 units, up 7.2% YoY, while detached houses decreased for the fifth consecutive month with 11,583 units, down 6.9% YoY. According to data released by Sanko Estate Co. at the end of April, the vacancy rate for large rental office buildings in the five central wards of Tokyo (Chiyoda, Chuo, Minato, Shinjuku and Shibuya wards) was 4.48%, down 1.1% on the previous month and the first decrease in three months. As in the previous month, the company's research forecast of a continued gradual decline, which had previously been predicted by the company, showed a gradual decrease this month, in line with forecasts, although it continued to rise last month and the month before last, contrary to forecasts. However, the vacancy rate is still likely to fluctuate between increases and decreases due to the effects of the stagnation of office relocation plans, particularly by foreign-affiliated companies, due to concerns over the economic downturn, and the tendency for relocation plans to take longer to materialise than before the Corona Vortex. The fact that March/April coincides with the end/beginning of the Japanese financial year is also thought to have had an impact on the decline in vacancy rates, so information from next month onwards will be of interest.

Table 2, New condominium for sale market trends limited to Tokyo and the three prefectures, shows a 2.1% decrease in the number of units supplied. This is the fifth consecutive month of decline, but for the first time in five months there was a single-digit rather than double-digit decline, although the downward trend is still continuing.

The number of remaining units was 5,189, down 263 units from 5,452 last month. The number of units supplied fell by 2.1% YoY to 2,439 units, but was the first increase in six months. The number of units supplied fell in all regions except Tokyo's 23 wards and Chiba Prefecture, where the contract rate rose 4.3% in the Tokyo metropolitan area, 8.8% in the 23 wards, 16.6% in Tokyo, 3.4% in Kanagawa Prefecture, 13.5% in Saitama Prefecture and 2.8% in Chiba Prefecture.

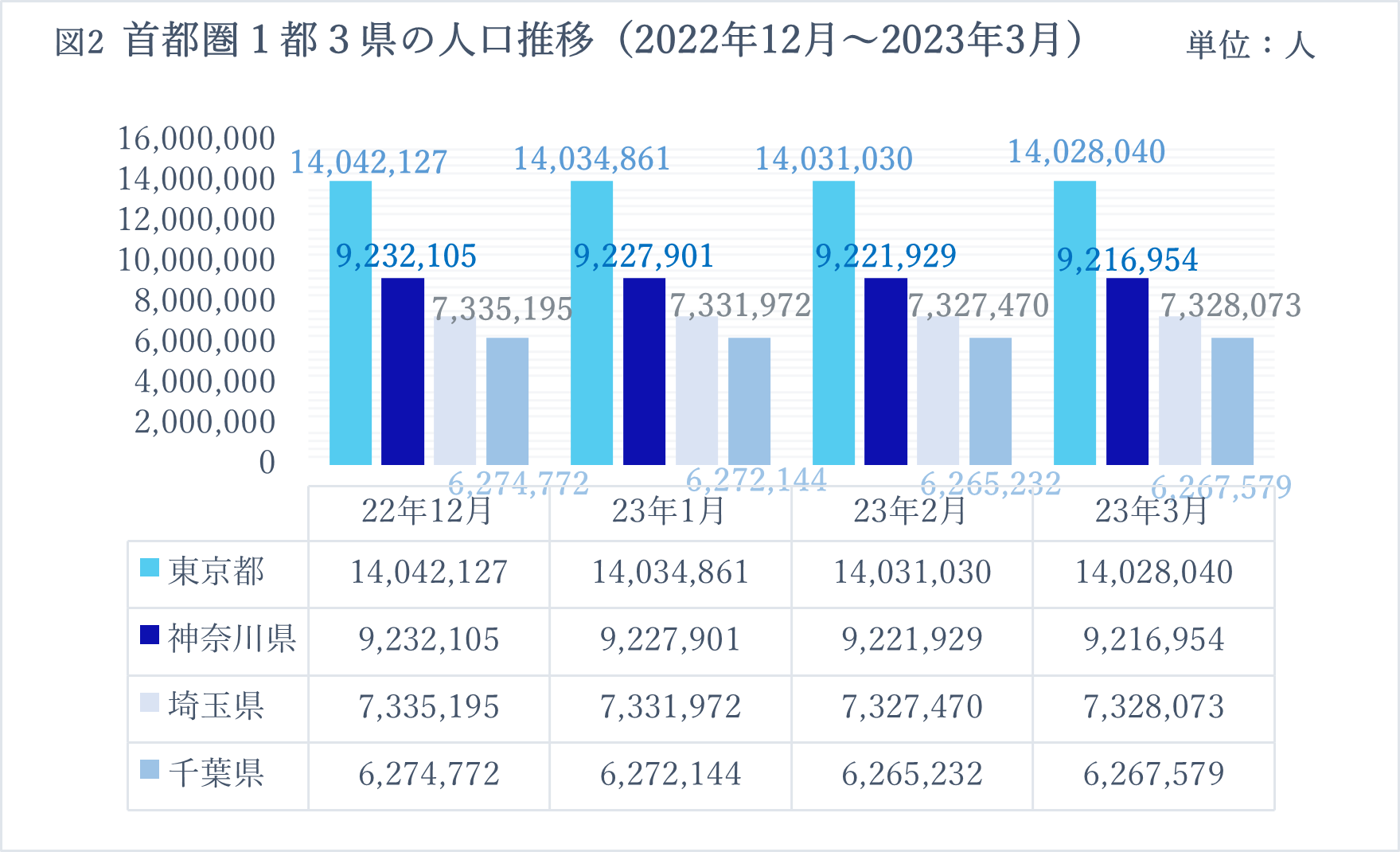

(Source: Prepared by the author based on demographic data from the Tokyo, Kanagawa, Saitama and Chiba governments / as of 22 May 2023).

Average sales price and price per square metre increased in all prefectures except Saitama Prefecture, where the contract rate for super high-rise properties with 20 or more floors was 90.4%, almost the same level as in the same month last year. The first-month contract rate in Tokyo and the three prefectures as a whole was 79.5%, marking the second consecutive month in which the rate was above 70%. The average price per unit was ¥ 143.6 million, a significant increase of 120.3% YoY and the first increase in two months. The price per square metre was JPY 1,023,000, the first increase in two months. The number of remaining units has decreased for three consecutive months, which can be seen as one indicator of the stability of the property market.

Figure 1, Population change: Tokyo saw its population decrease by 2,990 persons for the fourth consecutive month, while Kanagawa Prefecture also saw a decrease of 4,975 persons. On the other hand, Saitama and Chiba prefectures showed an increase of 603 and 2,347 persons respectively, the first increase in three months. This was the fourth consecutive month of excess out-migration in Tokyo. As we have seen over the last month, this downward trend is expected to continue, combined with the spread of telework, relocations out of the prefecture for risk dispersion and the expected expansion of the government's subsidy precision to encourage regional migration.

【3.Information on Property Market Trends: Economic Outlook】

In this section, the business climate pertaining to the property market is reviewed. First, macro data will be reviewed.

According to Table 3, National Consumer Price Index, the composite value decreased by 0.1% from last month to 3.2%, with the composite excluding fresh food remaining unchanged from the previous month at 3.1% and the composite excluding fresh food and energy increasing by 0.3% to 3.8%. As confirmed in last month's edition, the Government has been actively implementing price stabilisation policies on the occasion of the 7th meeting of the Task Force on Prices, Wages and Livelihoods, and the YoY increase was the 19th consecutive month of YoY growth, with the composite excluding fresh food and energy rising 0.3%, the same as in the previous month.

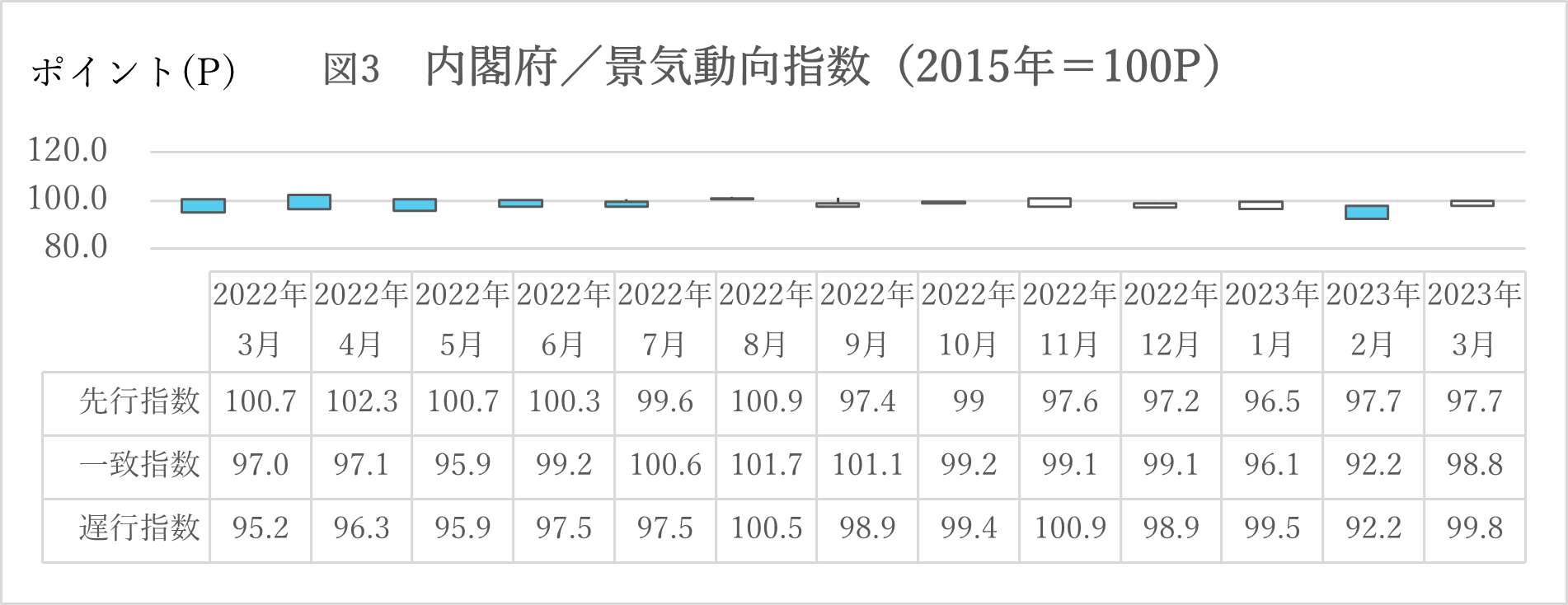

The following section looks at Figure 2 and the Cabinet Office Business Climate Index. The leading index was unchanged from the previous month by 0 points ('P'), while the three-month backward moving average (the high/low value calculated by comparing the figures for the month under study with the averages for December, January and February and January, February and March) fell by 0.7 points, the first fall in two months, and the seven-month backward moving average (the figures for the month under study with those for August, September, October and November) fell by 0.6 points, The seven-month backward moving average (the high/low value calculated by comparing the value for the month under study with the average for August, September, October, December, January and February and the average for September, October, November, December, January, February and March) fell by 0.59p, the 11th consecutive month of decline. The consistent index rose by 6.6p MoM, the second consecutive monthly increase;

The coincident index rose by 6.6p month-on-month, the second consecutive monthly increase. The three-month backward moving average fell by 0.13p, the sixth consecutive month of decline, while the seven-month backward moving average fell by 0.59p, the 11th consecutive month of decline.

The lagging index fell by 0.5p MoM, the second consecutive monthly decline; the three-month backward moving average fell by 0.06p, the first decline in 17 months; the seven-month backward moving average rose by 0.12p, the 13th consecutive monthly increase; and the three-month forward moving average fell by 0.06p, the first decline in 17 months.

The leading, coincident and lagging indices were unchanged and showed large increases respectively. The following section provides breakdown information showing a downward trend compared to the previous month. In the leading indices, the index of inventories of final demand goods decreased by 0.15%, the index of inventories of goods required for industrial production decreased by 0.26%, the number of new job offers decreased by 0.60%, real machinery orders (manufacturing) decreased by 0.08%, new housing starts decreased by 0.19%, the TSE stock index was unchanged at 0.00% and the small business sales outlook increased by 0.39%. The index increased by 39%. Matching indices showing decreases were the index of investment material shipments (excluding transport machinery), down 0.02%; commercial sales (retail trade), down 0.04%; commercial sales (wholesale trade), down 0.12%; effective job vacancy rate, down 0.24%; and the export volume index, down 0.07%. In contrast, the production index (mining) rose by 0.15%, the index for shipments of industrial production goods was unchanged at 0.00%, the index for shipments of durable consumer goods rose by 0.38%, the labour input index rose by 0.06% and operating profit rose by 0.01%. The lagging indices showed a 0.35% decrease in household consumption expenditure, a flat 0.00% in corporate tax revenue, a 0.38% decrease in the total unemployment rate and a 0.04% decrease in the consumer price index. Meanwhile, the tertiary activity index increased by 0.44%, the permanent employment index increased by 0.01%, regular payrolls increased by 0.25% and the final demand goods stock index showed an increase of 0.15%.

As a general comment, the Cabinet Office described business climate as 'at a standstill'. This is the fourth consecutive month that this expression has been used, suggesting that the economy may have entered a recessionary phase, so caution should continue to be exercised in future economic phases.

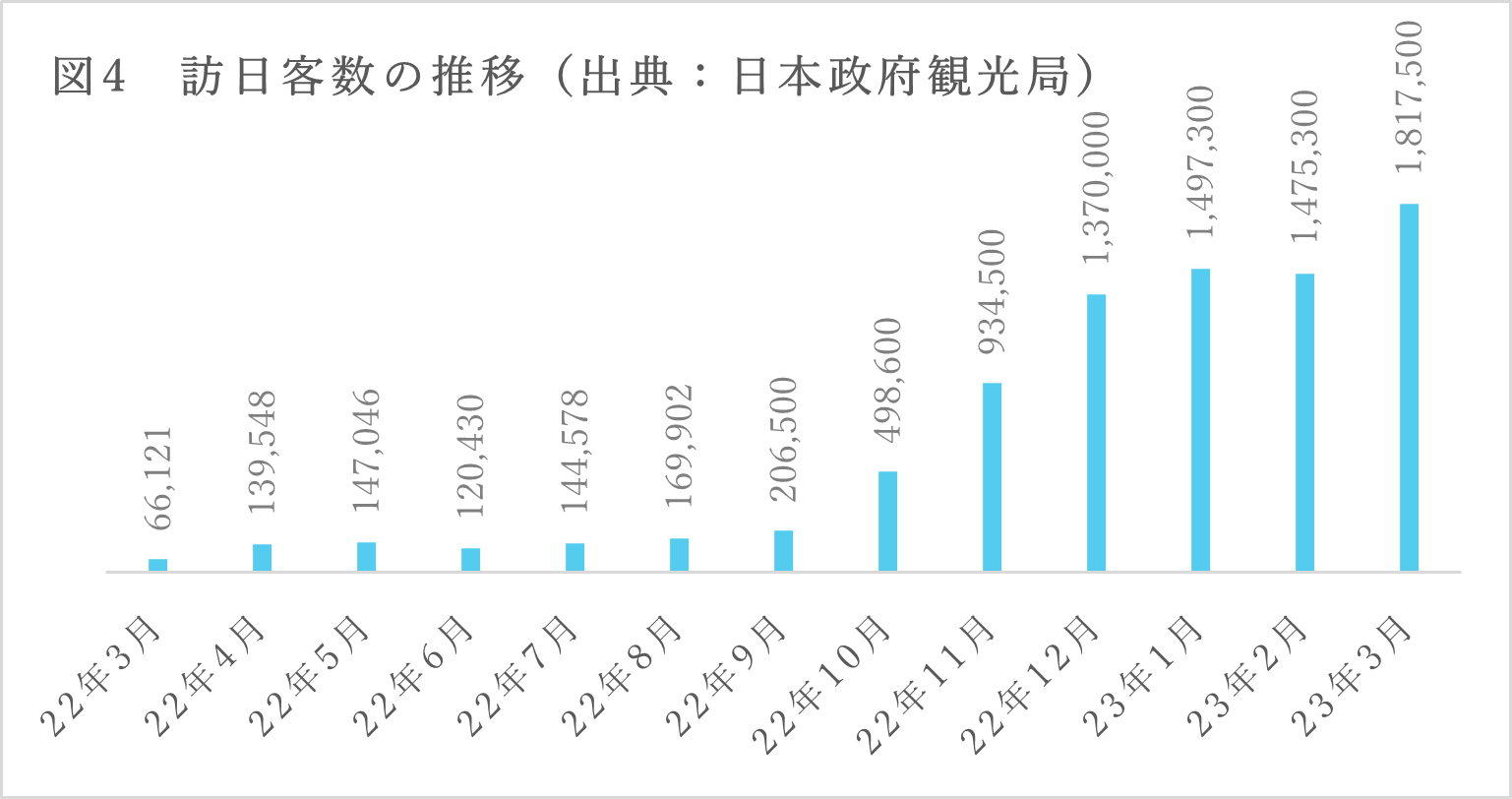

Figure 3 shows the number of visitors to Japan up to March this year. According to data released by the Japan National Tourist Organisation on 19 April 2023, due to high demand for visits to Japan during the cherry blossom season and the resumption of cruise ship operations, the number of visitors reached a level of 65.8% compared to the same month in 2019 before the Covid pandemic, the highest level since the resumption of individual travel last October. In terms of visitor nationality, there has been a significant increase in visits from the US, Europe, Australia and the Middle East, including the US. However, the situation is still not restored to the pre-Covid pandemic timetable, and many markets are still recovering as flights are being increased and restored. Furthermore, in accordance with the National Tourism Promotion Basic Plan approved by the Cabinet on 31 March, the Government has stated that it will strengthen its efforts to attract regional visitors, promote increased consumption, strengthen sales and information dissemination to overseas travel agencies and others based on cooperation with domestic stakeholders, and promote high-value-added travel and adventure travel. As a result of the above, a steady increase in the number of visitors to Japan is expected in the future.

【4.Prospects for Future Property Purchases】

Looking at exchange rate trends, the yen was at ¥139.80 as at 31 May this year (¥128.2 as at the same date last year), showing a stronger trend than before and a depreciation of about 8.3% against the yen as at the same date last year.

The outlook announced by the Bank of Japan on 28 April indicates that the upside and downside risks to the Japanese economy will remain relatively balanced, with a gradual economic recovery expected to continue until around the middle of the current financial year. However, the pace of growth is likely to slow towards the end of the period, and the potential impact of overseas economic and price risks on Japan's financial and exchange markets should be closely monitored. And the Bank will continue its 'Quantitative and Qualitative Monetary Easing with Long- and Short-Term Interest Rate Operations' measures with the 'price stability target' in mind until the actual YoY inflation rate exceeds 2% in a stable manner. If necessary, the Bank will not hesitate to take additional monetary easing measures.

In light of the BOJ's policy, the yen is expected to remain weak and, as in the previous issue, the current weakest yen in the last 30 years is still a good time to buy property using overseas assets.